How to Stay Compliant with Government Regulations in India

Running a business in India really comes with huge chances, but it also pulls in a bunch of legal duties. Whether you’re managing a startup, an MSME, an LLP, or a private limited company, staying compliant with the government’s rules in India is basically necessary if you want long-term success. Compliance isn’t just about dodging penalties; it is also about creating a more reliable, sustainable, and properly run enterprise.

Right now, businesses work in a regulatory environment that keeps changing fast. Tax laws, labour rules, corporate governance expectations, and even data protection requirements, are moving all the time. So companies that take business compliance in India seriously usually lower their legal exposure, and they also get a better reputation with investors, customers, staff, and yes, government authorities.

This detailed guide walks through the key regulatory compliance areas in India that businesses must pay attention to, and it shares practical moves to stay in line at each stage of growth.

Why Compliance Matters for Indian Businesses

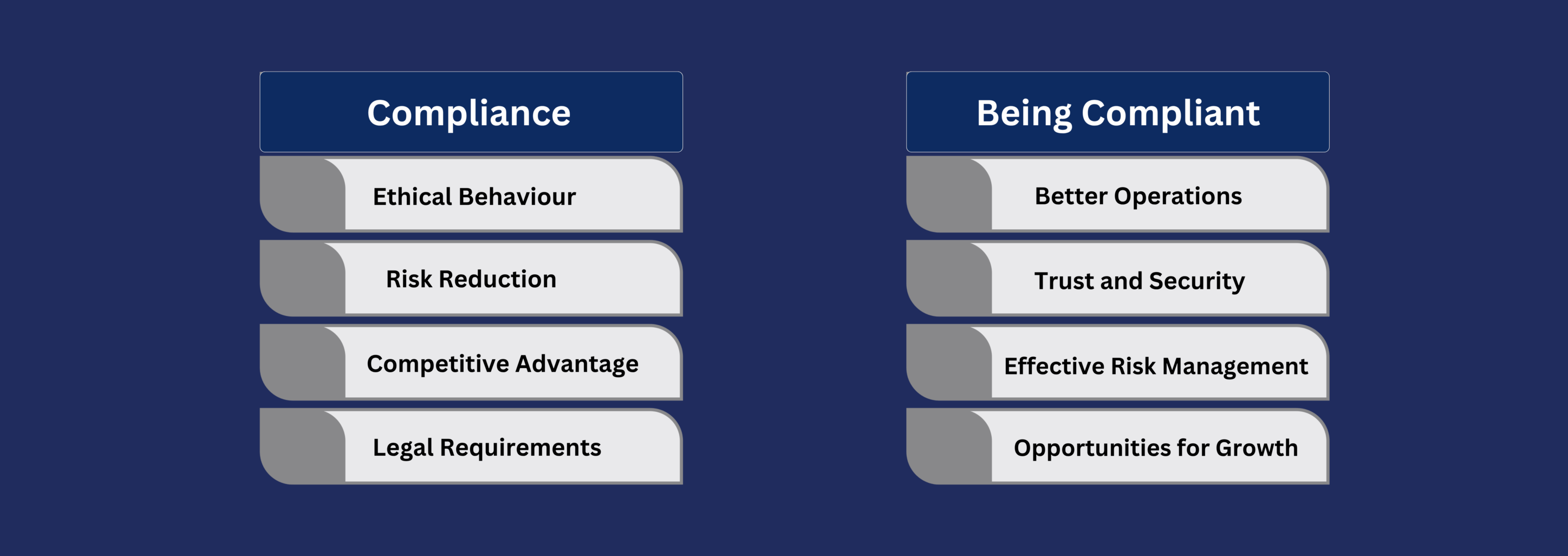

Many entrepreneurs think of compliance as an annoying box-ticking exercise. But, in fact, compliance is a business function that’s crucial for your success.

Ignoring India’s regulatory requirements can lead to penalties, license suspension, director disqualification, frozen bank accounts—and even imprisonment in the worst-case scenario.

Proper business legal compliance helps organizations:

- Avoid penalties, fines, and legal disputes

- Improve investor confidence

- Build customer trust

- Ensure smooth business operations

- Protect directors from legal liabilities

- Enhance brand reputation

- Support sustainable growth

Understanding the Key Areas of Compliance

To achieve effective company compliance in India, businesses must understand the major regulatory areas affecting their operations.

1. Corporate Compliance

Corporate compliance is governed primarily by the Companies Act and the Ministry of Corporate Affairs (MCA).

These obligations form the foundation of legal compliance for businesses operating as private limited companies or LLPs.

Businesses must:

- Complete company registration correctly

- Obtain Digital Signature Certificates (DSC)

- Maintain statutory registers

- Conduct board meetings

- File annual returns

- Submit financial statements

Important MCA Filings

Following these requirements ensures adherence to Indian business laws governing corporate entities.

- Form AOC-4 (Financial Statements)

- Form MGT-7 (Annual Return)

- Director KYC filings

- Event-based filings for changes in directors, registered office, or shareholding

2. Tax Compliance

Taxation remains one of the most critical aspects of statutory compliance India businesses must manage.

GST Compliance

Regular GST reconciliation helps prevent tax notices and improves cash flow management.

Businesses registered under GST must:

- File GSTR-1 returns

- File GSTR-3B returns

- Maintain invoice records

- Reconcile Input Tax Credit (ITC)

- Track supplier filings

Income Tax Compliance

Proper tax management is a core element of government regulations in India affecting every business.

Businesses must:

- File income tax returns on time

- Maintain accounting records

- Conduct tax audits where applicable

- Pay advance tax

- Deposit Tax Deducted at Source (TDS)

3. Labour Law Compliance

Employee-related obligations are among the most closely monitored Indian regulatory requirements.

Businesses operating in multiple states must understand that labour-related Indian business laws can vary significantly from one state to another.

Organizations must comply with:

- Minimum Wage Act

- Payment of Wages Act

- Shops and Establishments Act

- Employees Provident Fund (EPF)

- Employees State Insurance (ESI)

- Gratuity regulations

- Professional Tax regulations

4. POSH Compliance

POSH compliance is both a legal requirement and a vital part of creating a safe workplace.

The Prevention of Sexual Harassment (POSH) Act requires organizations with ten or more employees to do the following:

- Establish a POSH policy

- Form an Internal Committee (IC)

- Conduct awareness training

- Maintain complaint records

- Submit annual reports

5. Data Protection Compliance

With the Digital Personal Data Protection (DPDP) Act, businesses handling personal data must strengthen privacy controls.

Modern business compliance in India increasingly includes data privacy obligations.

Key measures include the following:

- Securing customer information

- Limiting access to sensitive data

- Establishing retention policies

- Implementing cybersecurity safeguards

- Training employees on data handling

12 Best Practices for Compliance Management

1. Digitize All Business Records

Physical files are difficult to manage and vulnerable to loss or damage.

Digital repositories simplify audits and support efficient compliance management in India strategies.

Maintain digital copies of:

- Incorporation certificates

- Tax filings

- Employee records

- Vendor contracts

- Licenses and permits

2. Create a Centralized Compliance Calendar

A compliance calendar is one of the simplest ways to improve company compliance in India. Track all monthly, quarterly, and annual deadlines in one place.

Include:

- GST filings

- TDS payments

- PF and ESI contributions

- MCA filings

- License renewals

3. Automate Compliance Processes

Automation significantly improves compliance management in India and reduces human error. Manual compliance tracking often leads to errors.

Use software solutions for:

- Payroll processing

- GST filing

- Employee management

- Compliance alerts

- Document management

4. Conduct Regular Internal Audits

Proactive audits strengthen overall business legal compliance. Quarterly compliance audits help identify risks before regulators do.

Review:

- Tax filings

- Payroll records

- Vendor compliance

- Corporate filings

- Employee documentation

5. Standardize Payroll Operations

Payroll accuracy is essential for effective statutory compliance in India. Payroll directly impacts EPF, ESI, TDS, and labor law compliance.

Ensure:

- Accurate salary calculations

- Timely statutory deductions

- Correct employee records

- On-time deposits

6. Monitor Vendor Compliance

Businesses can be held responsible for certain violations committed by contractors and vendors.

Vendor due diligence supports stronger legal compliance for businesses.

Before approving vendor payments, verify:

- PF deposits

- ESI contributions

- Labor compliance records

- Employee wage payments

7. Stay Updated on Regulatory Changes

Keeping track of government regulations in India helps businesses remain compliant and competitive. Laws evolve frequently.

Monitor updates from:

- Ministry of Corporate Affairs

- GST Council

- Income Tax Department

- Labour Departments

- Industry regulators

8. Develop Internal Compliance Policies

Strong policies create a culture of accountability and support India's regulatory compliance initiatives.

Document internal procedures covering:

- Payroll management

- Data protection

- Employee conduct

- Tax compliance

- Vendor management

9. Train Employees Regularly

Training strengthens compliance awareness across the organization. Compliance is not solely the responsibility of management.

Regular training helps employees understand:

- Legal obligations

- Workplace policies

- Data security requirements

- Reporting procedures

10. Focus on GST Reconciliation

Many businesses lose input tax credit because suppliers fail to upload invoices correctly.

This is a critical aspect of business compliance in India. Monthly GST reconciliation helps:

- Prevent tax disputes

- Improve cash flow

- Ensure filing accuracy

11. Understand Industry-Specific Regulations

Industry-specific Indian business laws must be carefully monitored. Certain industries must comply with additional regulations.

Examples include:

- FSSAI for food businesses

- RBI regulations for fintech companies

- SEBI regulations for listed entities

- IRDAI regulations for insurance firms

12. Consult Compliance Experts

helps ensure effective legal compliance for businesses and reduces compliance risks. No business owner can track every regulation independently.

Working with:

- Chartered Accountants

- Company Secretaries

- Legal Advisors

- Compliance Consultants

Consequences of Non-Compliance

Strong company compliance practices in India help organizations avoid these risks.

Ignoring Indian regulatory requirements can have serious consequences.

- Financial Penalties: Late filings and tax defaults can result in fines, interest charges, and penalties.

- Operational Disruptions: Authorities may suspend licenses or restrict business activities.

- Legal Liability: Directors and management may face legal proceedings for serious violations.

- Reputational Damage: Compliance failures can impact investor confidence, customer trust, and business partnerships.

How Technology Simplifies Compliance

Technology-driven statutory compliance India solutions reduce administrative burden while improving accuracy.

Businesses embracing digital transformation are better equipped to manage evolving Indian regulatory requirements efficiently.

Modern compliance solutions can automate many compliance functions, including:

- Deadline tracking

- Tax calculations

- Payroll processing

- Document management

- Audit preparation

- Regulatory updates

Conclusion: statutory compliance

Compliance is no longer only a legal duty—it is also kind of a business advantage. Firms that handle compliance early and manage it in real time tend to run smoother operations, win stakeholder trust, and end up with a solid base for future expansion.

When you digitizing records, automate key tasks, do regular audits, train team members, and keep pace with the shifting Indian business laws, you can move through the complicated regulatory environment with more confidence. It’s not just paperwork; it becomes day-to-day discipline.

Whether you are a startup, an MSME, an LLP, or a larger corporation, investing in effective compliance practices in India right now can save significant time, costs, and risks later on. Strong business legal compliance not only shields your organisation but also helps it grow sustainably in a world that is becoming increasingly regulated every year.

FAQs About statutory compliance

1. What is business compliance in India?

Business compliance in India refers to following all applicable legal, tax, labor, corporate, and industry-specific regulations required by government authorities.

2. Why is regulatory compliance important for businesses?

Regulatory compliance in India helps businesses avoid penalties, maintain operational continuity, build trust with stakeholders, and meet legal obligations.

3. What are the 3 C's of compliance?

The 3 C's of compliance are:

- Commitment – Leadership's dedication to following regulations.

- Communication – Clear policies and compliance training for employees.

- Control – Monitoring systems to ensure ongoing compliance.

4. What is compliance with government regulations?

Compliance with government regulations means following all laws, rules, and statutory requirements applicable to a business. This includes tax filings, labor laws, corporate filings, workplace safety standards, data protection requirements, and industry-specific regulations issued by government authorities.

5. How do businesses stay updated on regulatory changes?

Businesses stay updated through government portals, regulatory notifications, industry associations, legal advisors, chartered accountants, and compliance software platforms. Regular training sessions and periodic compliance reviews also help organizations adapt to changes in Indian regulatory requirements.

6. What are the 7 pillars of compliance?

These pillars form the foundation of an effective compliance management system. The 7 pillars of compliance generally include the following:

- Written policies and procedures

- Compliance leadership

- Employee training

- Effective communication

- Monitoring and auditing

- Reporting mechanisms

- Corrective actions and enforcement

7. What are the 4 phases of compliance?

This cycle helps businesses achieve continuous regulatory compliance. The four phases of compliance are:

- Assessment – Identifying applicable regulations.

- Implementation – Establishing policies and controls.

- Monitoring – Conducting audits and tracking compliance.

- Improvement – Addressing gaps and updating processes.

8. Why is statutory compliance important for businesses?

Statutory compliance helps businesses avoid penalties, maintain operational continuity, protect directors from legal liabilities, and build trust with customers, investors, and regulatory authorities. It also ensures smooth business operations and long-term sustainability.

9. What happens if a company fails to comply with regulations?

Noncompliance can result in financial penalties, interest charges, legal notices, suspension of licenses, director disqualification, reputational damage, and, in severe cases, criminal prosecution. Timely compliance helps businesses avoid these risks.

10. How can compliance management software help businesses?

Compliance management software automates filing reminders, document storage, audit tracking, payroll compliance, GST reconciliation, and statutory reporting. It reduces manual errors and helps businesses meet compliance deadlines efficiently.

11. How often should a business conduct compliance audits?

Most businesses should conduct internal compliance audits at least once every quarter. Regular audits help identify compliance gaps early, ensure adherence to Indian business laws, and reduce the risk of penalties during regulatory inspections.

Need Help with Compliance?

Let our experts guide you through the certification process.

Contact Us Today