10 Tax Compliance Tips Every Business Owner Should Know

Best Practices for Staying Tax Compliant Year-Round

Running a business means wearing, like, a dozen different hats: visionary, marketer, hiring manager, even customer service rep—and sure, sometimes you can sort of juggle them. But there is one hat you should never, ever take off: the tax compliance officer.

Tax rules keep moving, and the tax folks now lean on AI plus data analytics to cross-check what you file in real time, and honestly, the price of being wrong has been climbing and climbing. Whether you’re a solo freelancer or you’re growing past “just me,” staying sharp on tax compliance isn’t optional—it's the actual base layer for a stable business that stays mostly calm with penalties.

This guide gathers together the stuff a business owner truly needs, not the fluff: what tax compliance really means, who it applies to, the daily habits that help you avoid the audit trap, and a month-by-month checklist you can use every single time.

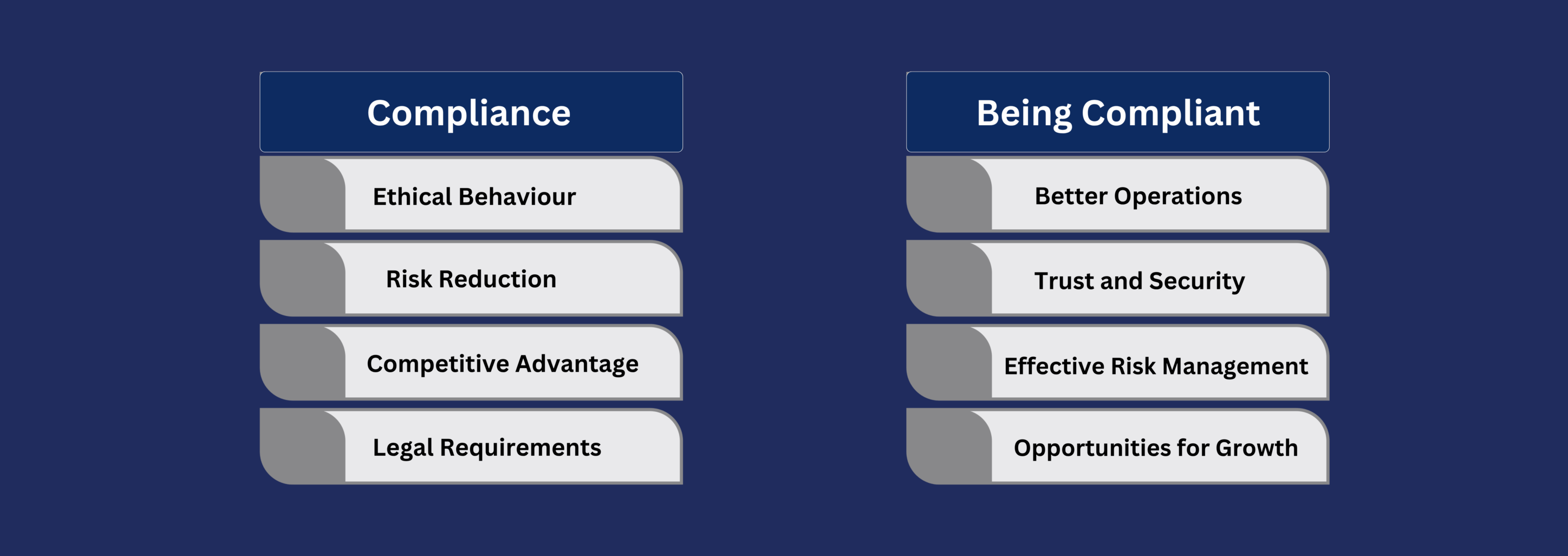

What Is Tax Compliance, Really?

At its core, tax compliance is really about accurately reporting your income, paying the right amount of tax, and filing everything on time—according to the guidelines set by your tax authority. In India, this is steered primarily by the Income Tax Act and increasingly by digital, automated matching systems that highlight any inconsistencies the moment they show up.

Being compliant isn’t only about dodging trouble. Solid tax compliance also means you understand which deductions and benefits you can claim, so you are never paying more than you legally owe. For registered companies, this fits into the wider world of corporate tax compliance, which includes its own routines, timelines, and reporting requirements.

Who Actually Needs to Worry About This?

Exemption limits vary by age: ₹2.5 lakh for individuals under 60, ₹3 lakh for senior citizens (60–80), and ₹5 lakh for super senior citizens above 80. If your income crosses these thresholds, filing isn't optional.

Tax rules apply more broadly than most people assume:

- Salaried employees who cross the basic exemption limit

- Self-employed professionals — doctors, lawyers, freelancers, consultants

- Sole proprietors and business owners paying tax on business profits

- Hindu Undivided Families (HUFs), treated as separate taxable entities

- Private limited companies, public companies, and foreign companies operating in the country are each subject to corporate tax compliance requirements under company law

Why Tax Compliance Matters More Than You Think

- Penalties add up fast. Late or incorrect filings attract both penalties and interest on the unpaid amount.

- Non-compliance invites scrutiny. Repeated errors can trigger audits and deeper legal complications.

- It signals financial stability. Clean records make it far easier to secure loans, visas, and business approvals.

- It funds public infrastructure. Taxes are the backbone of roads, healthcare, and public services—compliance is part of running a responsible business.

The Building Blocks of Tax Compliance

Together, these form the core of any solid business tax compliance system—miss one piece, and the rest starts to unravel. Get this right, and your annual business tax filing becomes routine rather than a scramble.

A handful of components make up the backbone of tax compliance in India:

- PAN (Permanent Account Number) — mandatory for every financial transaction and tax filing.

- Income Tax Return (ITR) filing — an annual disclosure of income, deductions, and taxes paid, typically done online.

- TDS (Tax Deducted at Source) — tax withheld at the point of payment, whether it's salary, interest, or a vendor invoice.

- Advance tax — paid in quarterly instalments if your total tax liability crosses a set limit.

- Self-assessment tax — any balance still owed after TDS and advance tax, settled before you file your return.

- GST compliance — regular, accurate filing of sales and returns for GST-registered businesses.

Practical Tax Compliance Tips for Business Owners

Here's the playbook that keeps businesses efficient, penalty-free, and firmly on the right side of the law.

1. Sever the Link Between Personal and Business Funds

Mixing personal and business expenses is one of the most common triggers for a tax audit. Paying for a family dinner from the business account or funding business software with a personal card creates a messy paper trail.

The fix: Maintain a dedicated business bank account and credit card. Pay yourself a formal salary or take structured owner draws, so every business tax filing clearly reflects genuine business activity.

2. Reconcile Constantly, Not Just at Year-End

Waiting until the tax year ends to sort your numbers is asking for chaos. True compliance depends on rolling, proactive checks between three pillars:

Books of Accounts ↔ GST/Sales Returns ↔ Income Tax Filings

Tax departments now automatically flag mismatches between reported sales and tax summaries. Keeping these three aligned protects your Input Tax Credit (ITC) from getting frozen and keeps unexpected notices off your desk. This is where strong GST compliance really pays off.

3. Digitize and Centralize Every Record

Keep digital and physical copies of profit & loss statements, balance sheets, invoices, and tax receipts for at least the legally mandated period — typically 6 to 7 years. Reliable accounting software (QuickBooks, Zoho Books, or similar) cuts down manual entry errors and keeps everything searchable when you need it most.

4. Stay Ahead of Regulatory Shifts

Tax frameworks evolve constantly — new forms, revised terminology, and stricter matching requirements are now the norm rather than the exception. If your accounting software or accountant hasn't updated to the latest rules, you're already behind. Choose vendors and suppliers based on how digitally compliant they are, since delayed invoice uploads on their end can block your input tax credit.

5. Plan for Advance Tax, Don't Just React to It

Waiting until year-end to settle your tax burden disrupts cash flow badly. Calculate and pay advance tax in quarterly installments to avoid interest penalties creeping in later.

6. Maximize Legitimate Deductions

Strong corporate tax compliance isn't just about paying on time — it's about not overpaying either:

- Depreciation on machinery, computers, and office furniture is often the largest legal cash-saver available to a business.

- Upskilling and training expenses for yourself or your team are increasingly deductible.

- Carried-forward losses — a rough financial year doesn't have to be wasted; losses can typically be carried forward up to 8 years to offset future profits.

7. Bring In a Qualified Professional

Tax codes are dense and constantly changing. Handing your bookkeeping and filing to a chartered accountant or tax consultant helps you legally maximize deductions while avoiding costly mistakes—which is especially valuable if you're managing tax compliance for small businesses with limited in-house finance support.

Your Monthly Tax Compliance Checklist

A receipt isn't optional — it's mandatory. If a deduction can't be proven digitally or physically, expect it to be disallowed during a routine check.

Breaking compliance into manageable, recurring tasks beats a frantic scramble every March. Use this as a running tax compliance checklist:

- By the 7th of every month — TDS deposit: Deposit tax deducted from salaries, vendor payments, or professional fees.

- By the 20th of every month — GST filing: File monthly GST returns, or track the QRMP quarterly cycle if turnover is under ₹5 crore.

- Quarterly — Advance tax review: Review profit projections and pay advance tax instalments on time.

- Annually, by July 31st — ITR filing: File your final Income Tax Return to preserve your ability to carry forward losses.

- Ongoing — Record-keeping: Store receipts and supporting documents for a minimum of 6–7 years.

GST Compliance Deserves Its Own Spotlight

For any GST-registered business, this is often where things quietly go wrong. Mismatches between GSTR-1 (sales) and GSTR-3B (summary returns) are now caught automatically, and a mismatch can freeze your input tax credit until it's resolved. Regular reconciliation — ideally monthly — keeps your GST compliance clean and your cash flow uninterrupted.

Common Tax Compliance Mistakes to Avoid

- Mixing personal and business finances

- Filing returns just before the deadline without reviewing them

- Ignoring updated tax regulations for businesses until a notice arrives

- Skipping monthly reconciliation and only checking books once a year

- Not backing up digital records or losing physical receipts

- Assuming a small business is too small to be audited

Do You Need Compliance Management Solutions?

As a business grows, spreadsheets and manual tracking kind of stop doing the job pretty quickly. Compliance management solutions—like accounting software, dedicated GST tools, or even a mixed setup that’s managed by your accountant—help pull everything into one place, keep deadlines in check, auto-calculate liabilities, and cut down on the little mistakes that often end up flagging audits.

If your business has multiple entities, operates across states, or you’re seeing high transaction volumes, then investing in the right tool(s) early usually pays back, like, a lot more than it costs.

Conclusion: Corporate Tax Compliance

Tax compliance shouldn't feel like this monthly game of defensive gymnastics, you know? If you keep your records clean, stay on top of the tax rules for businesses, run a steady tax compliance checklist, and treat your tax advisor like a year-round strategic partner, not just some emergency number you call at the last minute, then you end up protecting your cash flow and staying focused on what matters… growing your business.

Whether you’re just kicking things off or you’re scaling up, building strong business tax compliance habits right now can save you real money, time, and stress later. A clear, repeatable way of handling business tax compliance is one of the simplest competitive edges a growing company can put in place.

FAQs About Corporate Tax Compliance

1. What is the difference between tax compliance and tax planning?

Tax compliance is about accurately meeting your legal obligations—filing on time, paying the correct amount, and keeping proper records. Tax planning is the proactive side: structuring your finances to legally minimise your tax burden. The two work together, but compliance is non-negotiable while planning is strategic.

2. What are the biggest tax compliance tips for a new business owner?

Start with a dedicated business bank account, use accounting software from day one, reconcile your books monthly instead of yearly, and don't wait until a notice arrives to check your GST filings. These simple tax compliance tips prevent most of the common issues new businesses run into, and they lay the groundwork for solid corporate tax compliance as the business scales.

3. How is GST compliance different from income tax compliance?

It deals with indirect tax—filing regular returns on sales and purchases and ensuring your reported figures match your vendors' filings. Income tax compliance covers direct tax on your overall income or profits, filed annually. Both need to be handled, but on very different timelines.

4. What happens if a business misses its tax compliance checklist deadlines?

Missed deadlines usually mean interest and penalties on the outstanding amount, and repeated misses can trigger deeper scrutiny or audits. Persistent non-filing can also block your ability to carry forward business losses to future years.

5. Is tax compliance for small businesses really necessary if revenue is low?

Yes. Even modest revenue can cross exemption thresholds, and tax departments increasingly use automated systems that don't distinguish by business size. Tax compliance for small businesses matters just as much as it does for larger companies — arguably more, since smaller teams have less room to absorb penalties.

6. Do these tools replace the need for an accountant?

Not entirely. They handle the repetitive, calculation-heavy parts of the process—reminders, auto-categorisation, and reconciliation—but a qualified accountant still adds judgment, catches edge cases, and keeps you aligned with the latest tax regulations for businesses.

7. How long should I keep records for tax compliance purposes?

Most jurisdictions require retaining financial records — invoices, receipts, bank statements, and filed returns — for at least 6 to 7 years, since these documents may be needed during a future audit or discrepancy review.

Need Help with Compliance?

Let our experts guide you through the certification process.

Contact Us Today